Good Debt VS Bad Debt: What’s the Difference?

In a perfect world, everyone would be debt free.

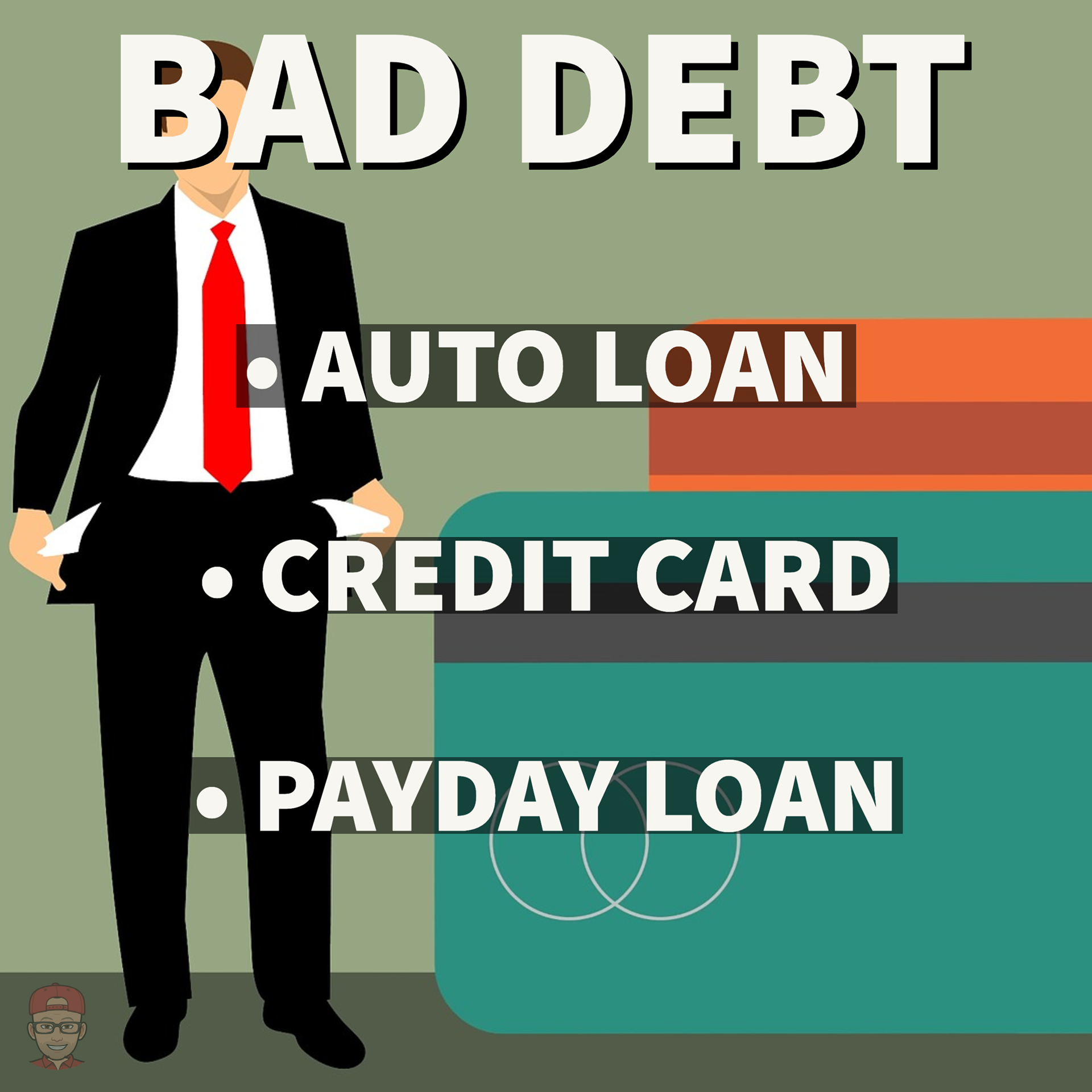

But debt is something most Americans are quite familiar with. Unfortunately, it doesn’t just disappear, and there is no magic wand to wave it away. Once you’re in debt, you’re in for the long haul. Keeping up with your payments is about all you can do. Well, aside from adding on even more debt in the meantime.

Adding Debt: When Does it Make Sense?

Is there ever a time when taking on additional debt makes sense? Absolutely.Think back to your first job fresh out of college. Would you have qualified for that role without your college degree? Either way, someone with a BA makes $500 a week more than someone with just a high school diploma. In other words, taking out a loan for college is an example of adding on good debt.

One way to think of good debt is in terms of return on investment (ROI). If you take out a loan and use it towards something that will boost your earning potential long-term—that’s good debt.

It isn’t just student loan debt that’s considered good. Debt from a mortgage loan, or a small business loan are also good. Owning property is an excellent investment, so a mortgage loan makes sense. In fact, the average sales price of a home has jumped over $124,000 in one year. How’s that for a solid ROI?

A small business loan is on the good side of the debt ledger too, because it can boost your wealth. But like all things in life, enjoy good debt in moderation. Too much good debt is, well, not great.

"If your loan pays for something that will boost your earnings and/or wealth in the long-term, this is considered a good debt."

Don’t Let Good Debt Go Bad

Good debt—if not kept in check—can spiral into bad debt. But this can be prevented if you follow a few simple tips.

• Keep good debt to a minimum. Too much good debt can sour fast. Debt is debt and even the good kind needs to be minimized.

• Don’t pay off debt with credit cards. Paying off debt while creating more debt doesn't make sense.

• Make your payments on-time. You lose control of your debt in a hurry when late fees and other penalties begin to pile up.One late or missed payment can snowball into an avalanche of overtures.

How to Avoid Bad Debt

Prevention is the key. Take the time to consider if this loan is really necessary. The key to debt managment is to stop taking out loans, even the kind that produce good debt.

• Evaluate the ROI. If this loan isn't for something that will add to your wealth, reconsider.

• Separate “wants” from “needs." Everyone wants a new car. And with good reason, as they smell awesome and look great. But you don't NEED a new car.

• Think long-term. To reduce anxiety, one trick is to keep your thoughts in the "now." To avoid debt, think not of now, but of the future. In five years you’ll just want a new car again. Resist the temptation, and focus on paying down your current debt instead. A new car today won’t help you in the future, but paying off your home loan will boost your wealth.

• Avoid impulse buys. Put that credit card back in your wallet or purse.

Remember that not all debt is created equal. But before you think about taking out a new loan, make sure that it's to pay for something that will add to your wealth, rather than just piling on more debt.